With so many bills putting pressure on our wallets, it might be hard to think about starting to save or invest your money seriously. Rent, cost of living, student loan payments—because all of these eat up your hard-earned cash fast, you may be waiting to save. Or maybe you have an established savings you’re looking to grow but aren’t sure where to start.

The good news? We offer several ways to help you save - no matter your level.

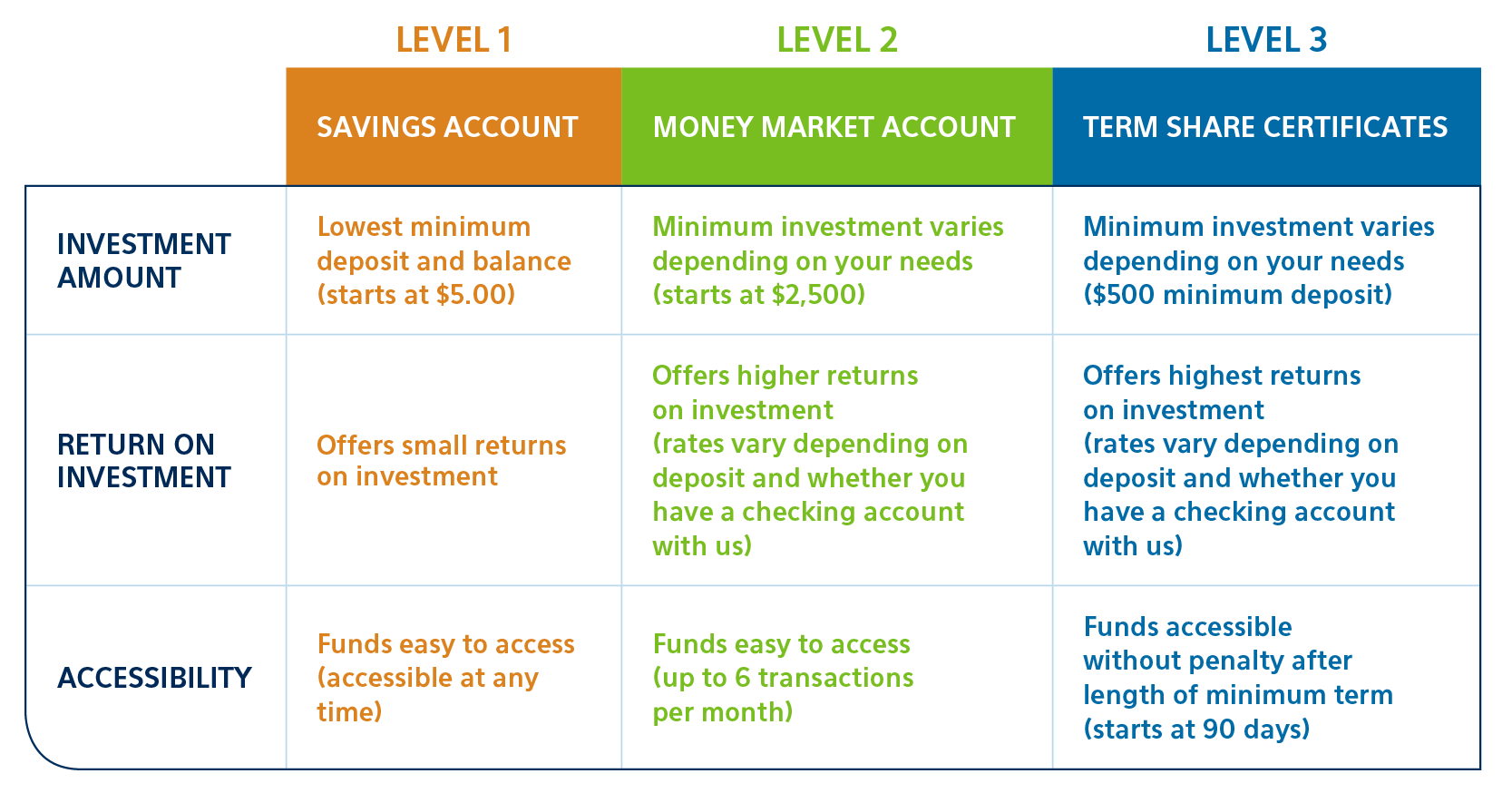

If you’re considering starting or growing your savings, various options depend on your personal goals and financial situation. Our Member Advisors typically share three popular accounts: savings accounts, money market accounts, and term share certificates. These accounts vary in interest rates, output, and accessibility to funds.

Savings accounts are separate from checking accounts and are meant for, well … saving. These accounts are used to put money aside to work toward a more significant financial goal. Generally, money in savings accounts earns interest or dividends, which means that the credit union will pay you interest on the money you deposit and leave in the account. Dividend and annual percentage yield (APY) rates for savings accounts are variable, which means they can go up or down at any time.

A money market account is similar to a savings account, but the main differences are return on investment and the level of access to funds. In money market accounts, you can still deposit and take money from the account at any time, but you’ll earn higher interest rates on the money you leave in (interest and annual percentage yield rates, like savings accounts, are still variable with money market accounts). Money market accounts can earn higher interest rates if you have a checking account with us.

A term share certificate is a type of savings or investment in which you put aside money for a pre-determined amount of time. Unlike savings and money market accounts, you receive a guaranteed rate for the term of your investment. However, you cannot withdraw your funds until the end of the term without paying an early withdrawal penalty.

Want to Save $$$? Pick Your Level...

Choosing the Right One for You

- Feeling indecisive? You can think of these accounts in terms of what we like to call “The Goldilocks Scenario.” A savings account is the Baby Bear of them all—great for getting your feet wet by saving money or setting aside funds for specific purchases or circumstances. Maybe you want to start small and put a few bucks away every month until you get that higher salary (our share savings account is an excellent option for that, requiring a minimum of just $5.00). Or, you want to go a little bigger and put chunks away for travel, an emergency, or even Christmas gifts (a sub-share savings account). These are all perfect scenarios for Unison’s savings accounts.

- Money Market Accounts, on the other hand, can be considered Mama Bear—they hold the middle ground between savings accounts and term share certificates. They work similarly to savings accounts—you can still deposit and withdraw your funds any time (up to six times a month)—but require a higher minimum deposit. They offer higher return on investment (ROI) than savings accounts, but you’ll generally get back a lower amount than term share certificates.

- Which brings us, then, to Term Share Certificates—the Papa Bear of the three accounts. These accounts offer the highest rates on dividends (but like Money Market Accounts, require higher minimum deposits than savings accounts). Term share certificates are good for long-term saving, such as for college or emergency funds, but your money must remain in the account for the duration of your chosen term. The Papa Bears are still low-risk in terms of investment accounts, and your funds are still relatively easy to access, but you won’t be able to reap the full benefits if you withdraw your funds early.

The Best Part

Ready to get started or need more information on ways to save? Consult the experts! Stop by one of our branch locations and meet with a Member Advisor to help you find the right fit.